After four years of work and 400,000 lines of code, Bank of America combines five different apps into one unified banking platform

- Bank of America recently combined banking, investing and retiring into one experience in a major update to its app.

- Dive into how the bank solved its Information Architecture challenges, reworked its personalization strategy, and introduced a new payments and transfer hub to formulate the new unified platform.

Bank of America recently combined banking, investing and retiring into one experience in a major update to its app. The bank’s managing director & product management executive, Jorge Camargo says the integration comes after the bank conducted extensive research and experience design studies that showed that their clients wanted “simplicity and convenience to monitor, manage, and optimize their full financial picture from a single place.”

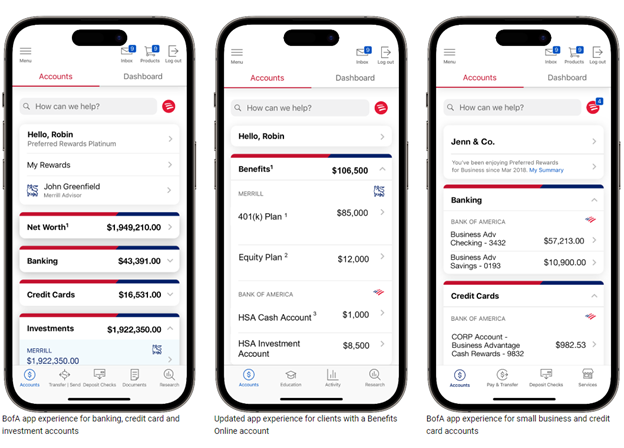

The unified platform integrates five different apps: Bank of America, Merrill Edge, MyMerrill, Bank of America Private Bank and Benefits OnLine. The new platform also integrates digital tools like LifePlan and Net Worth Estimator, as well as the bank’s virtual assistant, Erica.

Under the hood

The initiative took the bank four years to complete. The importance of building away from fragmentation and towards an integrated experience is highlighted even more when we consider that the bank’s digital experiences continue to be popular. Last year, the bank’s customers digitally interacted with their finances 23.4 billion times, which was an 11% increase year-over-year.

Any development and integration task at this scale starts with user research. Camargo adds that their Experience Design team’s work was “instrumental” to this initiative, concluding 125 research efforts with over 25,000 participants in the last year alone.

Building on this feedback, the bank now had to make its various apps and underlying architecture work together as one app. Here, Camargo adds that the biggest challenge was posed by “Information Architecture (IA) design and personalization capabilities”. That’s more easily said than done: BofA had to organize, structure, and label hundreds of digital features across disparate functions like banking, wealth, and retirement while prioritizing the ease of navigation.

The new app is now a single point of interaction regardless of the type of relationship a customer has with the bank, and although the content changes for different types of accounts (small business owner to credit card and investment accounts) the design features remain the same.

The bank intentionally staggered the roll out of its new app across 70 different releases to avoid disruption, according to Camargo. The completed app took 400,000 lines of code and 16,000 quality test runs, he said.

The two standout features of this new platform are its focus on personalization and the introduction of a “Payments and Transfer hub”.

Personalization: Consistent with the bank’s aim to provide an easy-to-navigate experience through its new platform, the bank had to build a personalization engine that gives clients access to the right information in the app.

This is best understood by zooming in on the research feature that is available to the bank’s clients in the app, which ensures that a credit card customer does not have access to equities research materials and a checking account customer is not uselessly faced with tools that can model the change in their retirement savings due to a difference in their 401(k) contribution.

Building capabilities that could understand the type of customer relationship and could surface the accurate experience and information is likely why Information Architecture (IA) was such a key focus for this project.

Payments and Transfer hub: The new app also has a dedicated payments-focused space, which allows customers to pay bills and receive domestic and international wire transfers. Customers will also be able to send international wire transfers in 140 currencies to 200 countries. “We want to make it as convenient as possible for clients to make and view all of their payments no matter how big or small, and the Payments and Transfer hub allows them to do just that,” said Camargo.

Along with these updates, the bank also expects its virtual assistant Erica to remain a critical feature of their user experience as their client’s in-app search engine.

“Bank of America continues to innovate and add hundreds of new features and capabilities every year, Erica will become the gateway for clients to discover and benefit from the digital features at their disposal,” said Camargo.